Degroof Petercam

on Multi Asset Class

Each time volatility rose in financial markets during the last couple of years, central bankers rushed to the rescue. This was the case after Bernanke’s Taper Tantrum, after the fall of the Renminbi at the start of 2016 and more recently after Brexit wreaked havoc on markets.

Also then, financial markets quickly congested this big event and moved on to the favourite pastime (or should we say ‘pass time’) of investment professionals and economists namely following central banks’ every move.

In that regard, several interesting observations spring to mind: firstly, the Federal Reserve decided not to hike rates in September blowing hot and cold on the state of the economy. Most likely, a next rate hike will come in December after the US presidential elections, which would bring the number of rate hikes to one each year. As such, the Fed remains on a very accommodative path.

Secondly, Mark Carney of the Bank of England, acknowledged that negative rates are not the answer and mentioned not to go down the road of Draghi, Kuroda and others. This is important because it limits additional moves of those latter central bankers into further negative territory.

A third point we noticed is that the Fed might be inclined to buy corporate bonds or equities instead of applying negative rates as Fed president Yellen indicated recently. It means that if a renewed slowdown would be around the corner in the US, financial markets will again receive additional support by central banks.

A fourth and final observation comes from the fact that an increasing number of voices are pleading for more fiscal stimulus next to the already extremely high and unprecedented level of monetary stimulus to support growth. Plans abound with Abe’s 4 trillion yen fiscal plan, Juncker’s EUR 630 billion investment plan and both US presidential candidates promising to lift infrastructure spending. Those plans can certainly help GDP growth if policy makers truly commit to find ways to implement it in an efficient way.

But will it be enough to seriously stimulate growth? The Fed recently lowered US potential GDP growth from 2.0% to 1.8%. In the not too distant past, that number used to be around 3%. Those monetary and fiscal packages are thus mainly meant to keep the economy afloat amid high burdens of debt and unfavourable demographic evolutions.

The next US president will find it a challenge to keep the economy from falling into recession. From a historical perspective, the current business cycle is already long in the tooth. The amount of stimuli described above should be sufficient to keep the economy in positive territory until at least the second quarter of 2017. As such, we remain cautiously constructive.

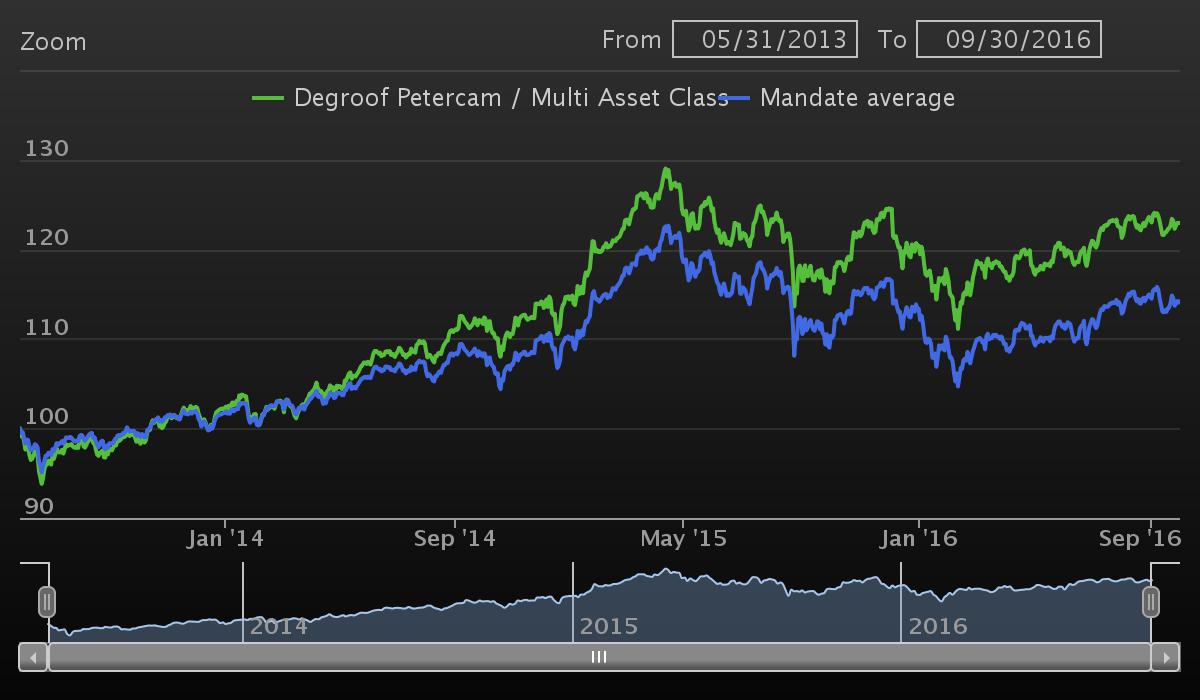

Multi Asset Class mandate on amLeague

This brings us to our AM League portfolio that has delivered an appealing 7-8% return annualized over the last three years with a volatility of 8.55% leading to a 0.80 Sharpe ratio. Not bad at all in the current low-rate, low-growth environment.

From the start onwards, we constructed a robust portfolio that would probably get the style ‘Diversified Growth’ attached in the UK. We focused on asset classes that are diversified without losing sight of the fact that we wanted deliver decent returns as well. The weight of equities has been lowered over the years, in line with the fact that they have become more expensive but the main themes are still alive and well: one such theme is to invest in equities worldwide and place sufficient low-risk bonds against them as long as correlation is low or even negative. The second theme was to invest in higher yielding bonds from emerging markets while balancing them out against the USD because emerging debt could be vulnerable to US rates and the USD moving up too quickly.

Source : amLeague, 30th september 2016

The same themes can be found in the fund Petercam L Patrimonial Fund, but in a somewhat more defensive way as the fund aims to keep the maximum drawdown limited to 5%. Up until now, the fund managers have been able to put this objective into practice. Not only through macro-prudential management and allocation of assets but also through selection of securities where the focus lies on selecting the best ideas of the house, be it on the equity side, or within corporate bonds.

Click here for the Petercam L Patrimonial Fund -F factsheet at 30th september.

|