| To view this news in your browser, please click here | |||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||

Outlook 2017: European equities

2017 could be a volatile year for European equities but this can create significant investment opportunities, particularly as earnings look poised to improve.

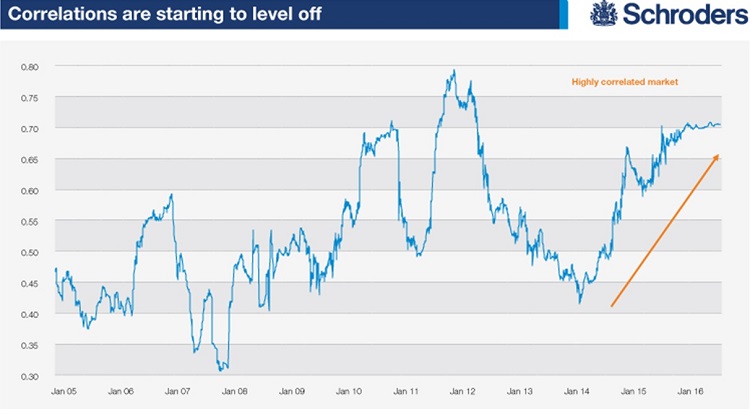

Uncertainty gives rise to opportunitiesMuch has been made of the deluge of elections due in Europe in 2017 and the uncertain investment environment that could result. We take the view that market uncertainty and volatility frequently present opportunities to buy good companies at attractive valuations. As active, long-term investors, the periods in which we can obtain the best returns are often those when others are most fearful. Alongside the various forthcoming European elections, the UK’s Brexit negotiations will be closely watched. We see Brexit primarily as an issue for the UK and do not believe it will have a significantly detrimental impact on corporate continental Europe. As an example, only 5% of EU exports go to the UK. Europe’s economic recovery remains slow but steady and we do not expect Brexit to derail this. Attractive valuations in EuropeAs ever with equities, the price you pay is a key determinant of the returns you can potentially make. In our view, European equities continue to look attractive from a valuation standpoint. The cyclically-adjusted price-to-earnings ratio1 currently stands at around 14x versus its 30-year average of 20x. We therefore feel Europe looks attractive relative to its own history as well as relative to other regional stock markets. Signs of earnings improvementOne reason why European equities have lagged other regions is that we have witnessed several years of earnings declines. Some of this has been due to pressure on the financial sector, as well as the effects of low commodity prices. However, we think 2017 could see European corporate earnings grow at their fastest rate in five years. Bond yields are indicating a pick up in inflation expectations, which is typically positive for an earnings recovery. The energy, commodity, utilities and chemicals sectors have seen positive earnings revisions over the last three months as year-on-year comparisons become easier and underlying commodity prices improve. We expect this trend to continue in 2017. Will correlations unwind?Rising inflation expectations and consequent improved earnings forecasts have seen value2 sectors (such as financials and commodities) start to claw back some of their underperformance versus quality sectors. Valuations in quality parts of the market - often perceived safe havens such as consumer staples - have become very extended in recent years. This outperformance of quality at the expense of value appears to be starting to unwind, and again this is another trend we see continuing in 2017. More broadly though, we hope that these kinds of thematic correlations between style groupings in European equities will start to wane, and there are some signs that this may indeed be the case (see chart below). The past few years have been largely driven by macro and momentum themes, with quality and growth parts of the market outperforming value. There has been little differentiation between stocks within those groupings and, in our view, this has led to the formation of new mispriced opportunities.

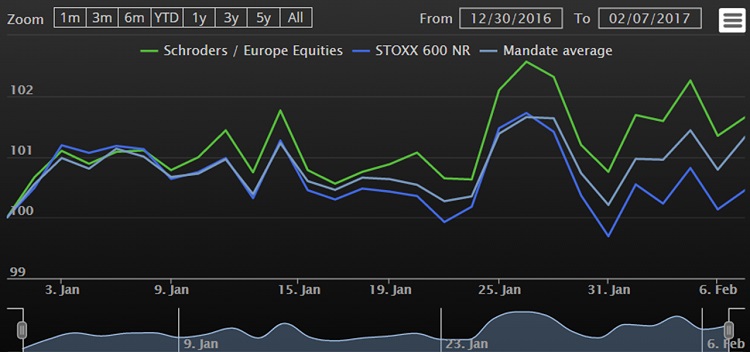

Source :Bloomberg. Schroders, as at 13 September 2016. Based on pairwise correlation of the Eurostoxx 50 index. 0 represents no correlation while 1 represents full correlation. Banks are an example of this highly correlated market as the whole sector has come under pressure amid low interest rates. However, there are very significant differences between individual banks in terms of capital strength, asset quality, cash generation and future dividend potential. An unwinding of correlations could allow those differences to be properly appreciated by the market. We feel it is prudent to be selective about exposure to banks. Favouring renewables and luxury goodsIn terms of specific sectors where we see opportunities, the renewables and alternative energy space is one we like. This covers a broad spectrum stretching from electric vehicles to wind power. This is an area where a long-term view is needed as changes in technology can take time to play out. However, it seems clear that the trend for greater electronic content in cars, including automated driving features, is one with scope to keep growing. In terms of wind power, this is another long-term structural theme. There has been some uncertainty over the prospects for the sector following Donald Trump’s US election victory. This has created some opportunities to buy stocks at cheaper valuations. We would also note that the switch to renewable energy is a global theme, not dependent on one country. Another sector where we see opportunities is luxury goods. Volumes in the sector were hit hard by the Chinese clampdown on gift-giving by public officials and valuation levels for several stocks now look compelling. We see significant recovery potential and a number of factors can lend support. Specifically, we would highlight the ongoing increase in global travel and tourism, greater access for luxury firms to growth markets, product innovation, and a pick-up in firms’ ability to raise prices if inflation does indeed return. We would also point to the role of technology here and many luxury firms have not yet taken full advantage of the potential offered by e-commerce. Conclusion – opportunities amid volatilityIn summary, the political environment in 2017 looks set to create further volatility which we believe will create significant investment opportunities given the probable sentiment swings in the market. Valuations remain compelling and the slow economic recovery in Europe should provide a solid backdrop for corporate earnings to deliver potentially their best growth rates for five years. Correlations are at elevated levels although there are signs that the momentum is changing driven by the pick up in bond yields. We remain highly vigilant in our search for mispriced opportunities (particularly during volatile market conditions) as earnings growth should differentiate company performance over the coming months. SCHRODERS on amLeague Europe EquitiesThis strategy has successfully been implemented since the beginning of the year on the Europe Equities portfolio managed on amLeague, with an outperformance of 1.20% ( On Feb 7, 2017, YTD performance of 1.65% vs 0.45% for the Stoxx 600 Europe)

1 The cyclically-adjusted price-to-earnings ratio is defined as price divided by the average of ten years of earnings (moving average), adjusted for inflation. 2 A value stock is one that tends to trade at a lower price relative to its fundamentals (e.g., dividends, earnings and sales) and thus considered undervalued by a value investor.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions

which may change. We accept no responsibility for any errors of fact or opinion and assume no obligation to provide you with any changes to our assumptions or

forecasts. Forecasts and assumptions may be affected by external economic or other factors. The views and opinions contained herein are those of Schroder Investments

Management’s European Equities team, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

amLeague |

|||||||||||||||||||||||||||||||||||||||||||||||||

| If you no longer wish to receive amLeague newsletters, unsubscribe here | |||||||||||||||||||||||||||||||||||||||||||||||||