Investing in the New Digital Economy

By Lucy Macdonald

CIO Global Equities

The internet has been with us for decades. For investors, global technology giants dominate the top ten market capitalisations. Yet the Digital Economy’s transformation of the corporate sector is still at a relatively early stage.

We are all aware of the digital heavyweights which have become so familiar in our daily lives. However, the Digital Economy phenomenon goes well beyond the formation of new online businesses. It also includes the shift of existing corporates online, with all the cost, business model and cultural disruption that this entails.

From a technological standpoint, the changes are being driven by three things: the ubiquity of mobile internet access, increased broadband capacity and the availability of cloud storage. At the same time, consumers are demanding an ever-greater range of services. This is intensifying competition and with it, the pace of change.

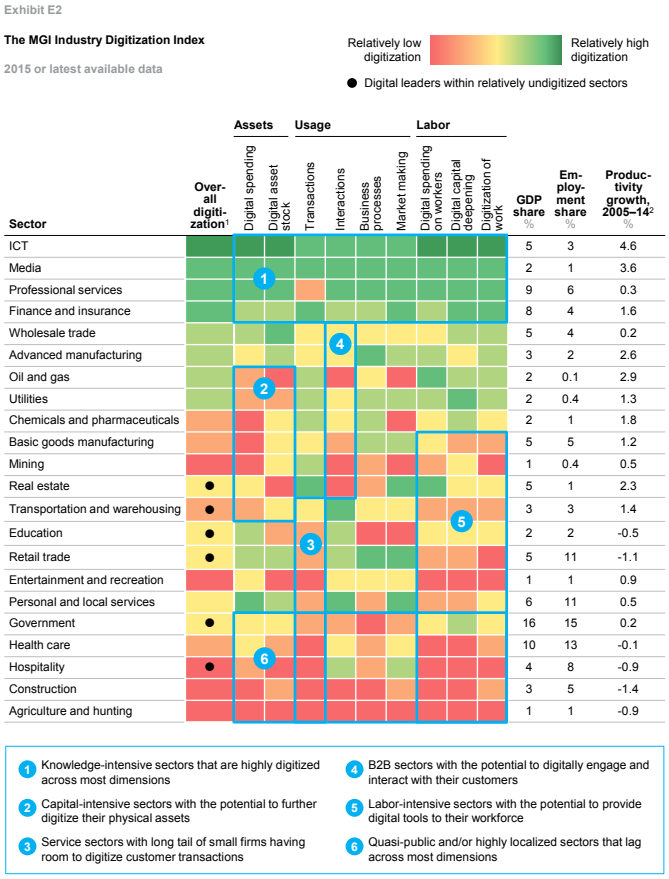

In response to this, the McKinsey Global Institute has compiled an index that assesses to what extent companies are embracing digital technology. The study gauges how much companies are investing in digital assets, the manner in which they are being used, and how their workforces are being taught to use this technology. The conclusions are stark.

Top companies in leading sectors have workforces thirteen times more digitally engaged than the rest of the economy. Furthermore, when comparing the US as a whole to its leading sectors, the Institute concludes that the economy is operating at just 18% of its digital potential. If we assume that the digitalisation of our global economy will encompass most industries over time, this transformation could last for several decades more.

Yet this very transition creates one of the biggest challenges for modern investors: how does one appropriately analyse and value companies in the new economy?

It is increasingly clear that new economy assets are not being measured or recognised accurately. As a result, one of the greatest challenges for fundamental analysis is the extent to which accounting for the digital world lags reality. Corporate focus has shifted from making long-term capital investments to spending on flexible, usage-based operating systems. This trend explains the rapid growth in cloud-service offerings launched by the likes of Amazon, Google, and Microsoft. From an accounting perspective, this means Operating Expenditure (Opex) is taking the burden traditionally carried out by Capital Expenditure (Capex).

Meanwhile, over the past decade, Research and Development (R&D) in the quoted sector has steadily come to exceed Capex as a percentage of assets. Under United States Generally Accepted Accounting Principles (GAAP) R&D has to be expensed, based on the traditional argument that benefits from R&D are more uncertain than Capex. Recent evidence is undermining this argument but the practice remains, potentially understating asset bases while distorting profitability and return on equity.

Valuing the digital workforce is even more problematic than valuing digital assets. Human capital – the data analysts and engineers so vital to the business – are treated as costs against profits, rather than as revenue-generating assets. In assessing their contribution therefore, more granular data is required. What’s more, if an estimated 47% of jobs are susceptible to computerisation, companies will be increasingly susceptible to internal disruption, as a type of digital apartheid develops between technologically enabled and automatable roles.

Valuation is always a mixture of art and science, but in this era, even more art is required. Technological innovations often have network effects associated with them, leading to greater scale and margin divergence. The extremes to which company values can go has risen as the outcomes between immense scale and profitability or corporate ruin have diverged. Today there are seven companies with market capitalisations over $400bn. Ten years ago, there was only one (ExxonMobil). And unlike a decade ago, all except one of these (Berkshire Hathaway) are technology enabled.

The impacts of these developments on active investors are profound, from asset allocation to sector and stock analysis. Indeed, the investment profession itself is being transformed by technology, creating the need to combine high quality thoughtful fundamental analysis with new digital tools and data sets.

At a country level, the US and China are leading in the digitalisation of consumer industries. Between them, these two countries have created some of the world’s leading online companies including Facebook, Tencent, Alphabet and Alibaba. However, in the manufacturing space, Europe, Korea and Japan, may be among the most well-positioned to capitalize on digitalisation. These regions already boast world-leading manufacturing operations and are likely to benefit from the efficiency gains digitalisation offers. Conversely, for many emerging markets, digitalisation could pose a threat to their long-term economic fortunes as more advanced automation means manufacturing can be “reshored” to the consumer’s home market.

Digitalisation also presents an increasing array of Environmental, Social and Governance (ESG) issues for investors. Technology-enabled companies can go from start-up to mega-cap at breakneck speed: typically 5 years compared to 20 for the average company. This puts tremendous strain on the development of corporate culture. In some cases, ownership structures, pay and voting rights for globally dominant companies are virtually unchanged from start up. This can lead to the type of problematic corporate behaviour – and ensuing regulatory retaliation – we have seen at the likes of Uber, Google and Amazon.

The maturity of the Digital Economy is still at an early stage. As the significant investment phase ends, digitalisation’s disruptive challenges will start to be outweighed by the corresponding rise in productivity gains. In the meantime, company fortunes are diverging more than ever before.

For active managers, this creates ideal opportunities for higher alpha generation. It is vital to pick those companies that are leading, and profiting from, the digitalisation trends in their industries, while at the same time avoiding the losers. These well-positioned companies may attract valuation premia for longer than usual, testing sell disciplines. Correctly identifying and valuing those companies best-positioned to seize the opportunities digitalisation brings will determine relative investment performance for years to come.

References:

https://hbr.org/2016/04/a-chart-that-shows-which-industries-are-the-most-digital-and-why

https://hbr.org/2016/01/the-most-digital-companies-are-leaving-all-the-rest-behind

|