Please wait...

Please wait...amLeague_INDEXING

Methodology

Trading at Close NAVs:

To calculate the Trading at Close NAV of a portfolio, all trades are calculated by multiplying the quantities traded by their closing price.

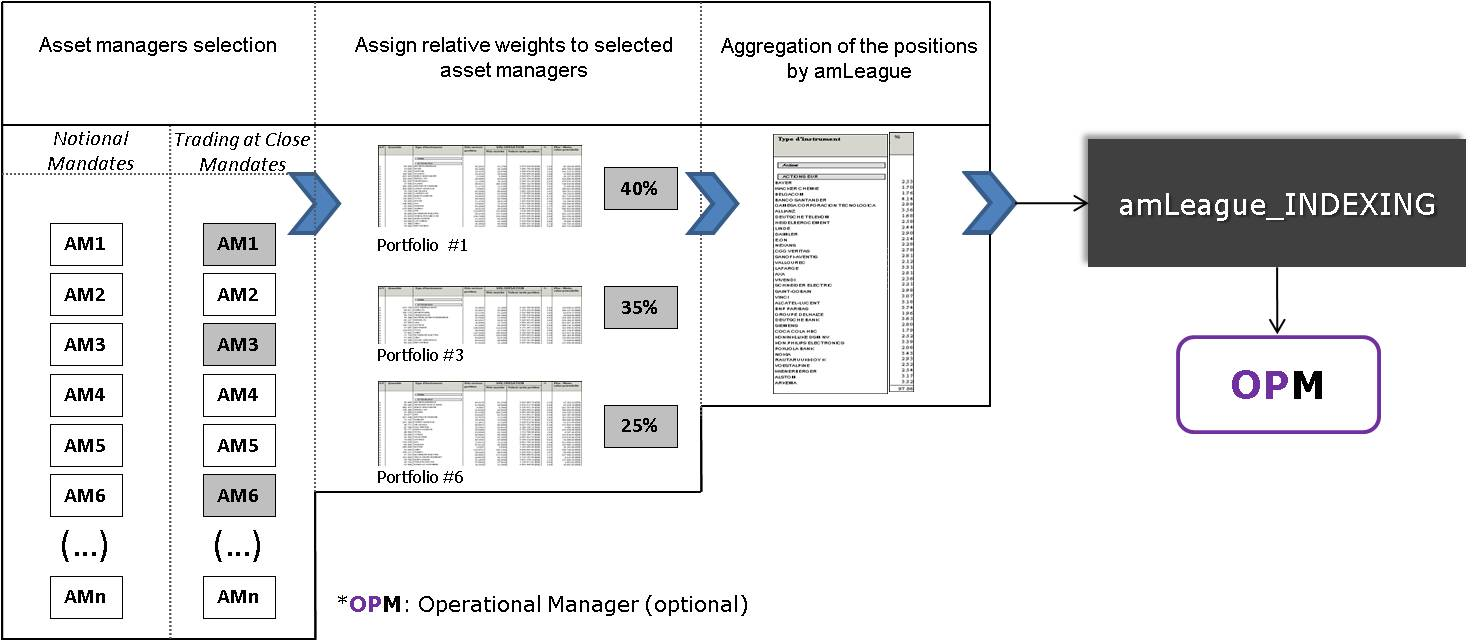

Creating a strategy or an index:

The creation is a 4-steps process:

1. Analysis: commissionned to amLeague by the Index Sponsor (investor / product manufacturer).

2. Selection of the underlying asset managers on amLeague platform or by invitation if the asset manager is not already on it. A weight is assigned to each mandate, representing its percentage in the index composition. The total of these weights must equal 100.

3. Aggregation: at inception, the relative weights of the securities held in the undelying portfolios are multiplied by the weight assigned to each asset manager retained in the index composition in order to obtain the percentage of each security in the index. The index value is calculated on the a daily basis with closing prices.

4. Replication:

- Strategy: once per day, a file summarizing the aggregate positions of the strategy is sent to the operating manager who executes orders at close prices on the replicated index in order to minimize the tracking error between the index and the final financial product. amleague only sends the aggregated weight of undelying asset managers and therefore respects the privacy of each asset manager'holdings.

- Index: the index composition is reshuffled once a month. However, corporate actions are processed within the month. The index is valued on a daily basis and is published on amleague website.